The Persistence of Position

How Wealth Accumulation Becomes a Self-Perpetuating System

Ranchhod, V., Jana, A., and Keshav, A. V.

SALDRU, University of Cape Town

9 November 2025

Introduction: From 'Sticky' to 'Self-Reinforcing'

The first post in this series discussed the fundamental difference between income (a flow) and wealth (a stock), and suggested that wealth distributions are more “sticky" and persistent. Using 2017 comparative data, it illustrated the differences in net personal wealth between countries like South Africa and Brazil on the one hand, and Germany and the United Kingdom on the other.

This post posits that this “stickiness” is not a passive phenomenon. It is an active, self-reinforcing system powered by potent economic and political mechanisms that actively concentrate capital at the top of the distribution. Wealth is not just persistent; its accumulation is self-perpetuating. Understanding these dynamics of accumulation are essential for evaluating the policies designed to challenge it.

The Engine of Accumulation: r > g and Scale-Dependent Returns

The persistence of wealth is driven by self-reinforcing feedback loops. The primary macroeconomic driver, identified in the works of Piketty, is the relationship r > g. (Piketty, 2014)

This formula states that when the average rate of return on capital (r) consistently exceeds the rate of economic growth (g), wealth inequality will mechanically rise. Economic growth (g) represents the new value created in the economy, primarily through labour (income). The return on capital (r) represents the growth of existing wealth (stock). When r > g, it means that wealth accumulated in the past (capital) grows faster than the economy as a whole. The inevitable result is that inherited fortunes come to dominate wealth created through work, and the share of wealth held by capital owners pulls away from the rest of society.

This dynamic is further amplified by a critical feature of modern economies: scale-dependent returns. The rate of return, r, is not a single, uniform number for everyone. The very state of being wealthy grants access to asset classes that generate higher returns, while the less wealthy are confined to lower-return assets.

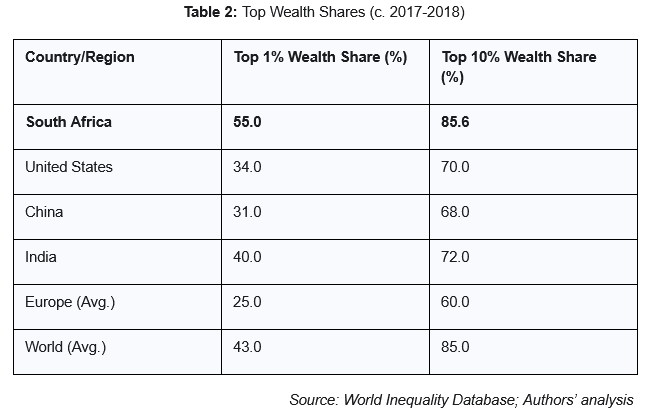

In South Africa, for example, the bottom 90% of the population holds the majority of its assets in relatively low-return categories like housing and pension funds. In stark contrast, the top 1% owns over 95% of all high-return bonds and stocks in the economy (Chatterjee et al., 2022).

This structural difference holds across all our sites of study. Portfolio composition creates an endogenous feedback loop (World Inequality Database, n.d.):

An individual near the median in Germany (avg. $133,052) may invest in a safe, low-yield public bond or a savings account, but will that be significantly higher than someone near the middle in South Africa (avg. $ 5,962.08)?

An individual with average top 1% wealth in South Africa (avg. $2.44 million) has access to private equity, hedge funds, and bespoke financial instruments that offer far higher returns; but is that similar to what the 80-90th percentile in Germany receives?

It is not just that wealth grows; more wealth grows faster. We posit that the dynamic is not only r > g, but also r(top 1%) > r(middle 40%), and further, that this might vary by location, i.e., r(top 1% in Germany) ≠ r(top 1% in South Africa).

The Rules of the Game: Stiglitz, Rent-Seeking, and the Political Construction of r

If r > g is the economic engine, political forces provide the micro-foundations that keep it running. Joseph Stiglitz’s concept of rent-seeking argues that today’s extreme inequality is not an inevitable or natural outcome of capitalism, but the result of the wealthy using their financial power to capture the political process (Stiglitz, 2011, 2012; Stiglitz et al., 2015).

“Rent-seeking” is the practice of shaping rules, regulations, and tax codes to one's own benefit, allowing one to extract more wealth (rent) from the economy without producing more value. This includes lobbying for preferential tax treatment of capital gains over labour income, creating barriers to entry for competitors, and securing state subsidies or contracts.

This political influence is the mechanism through which r is kept artificially high and protected from taxation. Stiglitz’s work suggests that Piketty’s r > g is not a natural law of economics; it is a politically constructed and maintained reality.

This theory finds practical confirmation in the very methodological challenges of studying wealth. HNWIs are notoriously difficult to capture in survey data, are less likely to respond, and utilise offshore tax havens and "astute estate planning" to limit tax liabilities (Lustig, 2020; Saez, 2017; Zucman, 2019).

This is not merely a data problem for economists; it is the empirical evidence of Stiglitz’s rent-seeking in action. The opacity of capital, enabling the "missing wealth of nations," is a direct consequence of political choices that protect r from taxation and public scrutiny. The outcome of these accumulation dynamics is a level of wealth concentration that is staggering, particularly in South Africa, which stands as a global outlier.

The Global Policy Counter-Movement

This reality—of extreme, politically-maintained inequality—has become so stark that it has forced its way onto the global policy agenda.

In 2024, this debate has been championed by the G20, under the presidency of Brazil. Brazil's finance minister, Fernando Haddad, has made a global minimum tax on billionaires a central theme, urging G20 counterparts to "ensure that the world’s billionaires contribute their fair share in taxes" (Partington, 2024).This move aims to build on the recent global minimum tax on multinational corporations, tackling the "hypermobile" nature of personal billionaire wealth (Cohen, 2025; Walt, 2025; Zucman, 2024).

It is no coincidence that this charge is being led by countries from the global South. As noted by Piketty, the decision by South African President Cyril Ramaphosa to place inequality at the heart of the G20 agenda was "historic" (WID.world, 2025). This push from the IBSA nations (India, Brazil, South Africa) reflects a growing recognition that tax and social justice are prerequisites for development (DIRCO, 2025). This political momentum is backed by a G20-commissioned report on global inequality, led by Joseph Stiglitz himself, which advocates for an International Panel on Inequality (IPI) modeled after the IPCC to systematically track inequality and its causes (Stiglitz et al., 2025b, 2025a).

National Frictions and the 'Millionaire Flight' Myth

While the G20 discusses this at a global level, the national debates within our project’s sites of study reveal the intense political friction and powerful narratives used to resist such changes.

The United Kingdom serves as a prime case study. In late 2024 and 2025, the new government, facing a significant fiscal gap, has been forced to confront tax policy head-on. However, the debate is not a simple "yes" or "no" to a new wealth tax. During a House of Commons Treasury Committee session, tax experts warned against the complexity of introducing new wealth taxes (House of Commons, 2025). Instead, they advocated for reforming existing capital taxes (like inheritance tax or capital gains) to be less economically damaging and more efficient, rather than adding new, complex layers (Institute for Fiscal Studies, 2025).

This technical debate is occurring against the backdrop of a fierce media narrative centered on "capital flight." In 2024, reports emerged that a massive "millionaire exodus" from the UK of 9,500 individuals–this narrative was immediately weaponised to argue against any tax increases on the wealthy. However, a follow-up study debunked this narrative as a "myth" –they pointed out that the 9,500 individuals represented just 0.3% of the UK's 3 million millionaires. Furthermore, they highlighted that academic studies consistently show that tax-motivated migration among the wealthy is minimal. This reveals a critical aspect of the modern inequality debate: policy discussions are often held hostage by a political narrative of capital flight that is not supported by empirical evidence. The existence of groups like the "Patriotic Millionaires," who are actively lobbying to be taxed more, further complicates the simplistic idea that all wealthy individuals will flee (Tax Justice Network et al., 2025).

Simulating a Stubborn System: The 'Policy Time Machine'

Given this sticky, self-reinforcing system—and the political narratives surrounding it—how can policy effectively intervene? The global debate has coalesced around wealth taxation, but a critical question remains: what can it actually achieve?

To answer this, traditional equilibrium-based economic models are often inadequate. Such models typically rely on a "representative agent" that "averages away" the very diversity and extreme heterogeneity that is the hallmark of an unequal society. They are fundamentally ill-equipped to model a system defined by its extremes.

A more suitable approach is offered by Agent-Based Models (ABMs). An ABM is a bottom-up computational method that creates a "virtual laboratory". Instead of one "average" agent, the model simulates a large population of heterogeneous agents, each with unique attributes including wealth, income, and savings rates. These agents interact according to a set of rules, and the macro-level distribution of wealth emerges organically from these micro-interactions over time.

The true value of an ABM in this context is its function as a policy time machine. The dynamics of wealth accumulation and the effects of policy unfold over decades and generations, a timescale far beyond any single election cycle. An ABM allows researchers to simulate 100 years or more of policy impact in a short time frame, making the long-term consequences of today’s decisions visible and helping to overcome the "political short-termism" that often plagues structural reform.

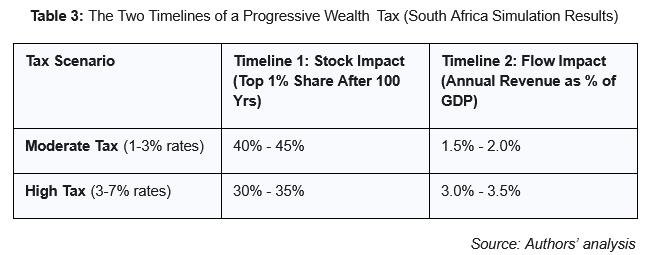

A Tale of Two Timelines: The Policy Paradox of a Wealth Tax

As part of our ongoing research, we are developing agent-based models to simulate the accumulation and distribution of wealth for a synthetic population whose initial demographic and economic characteristics are derived from South Africa's National Income Dynamics Study (NIDS). The model specifies rules for how individual agents earn stochastic labour income, gain differential returns from a portfolio of capital assets, and experience wealth-dependent demographic changes such as fertility and mortality. The framework also accounts for the intergenerational transfer of wealth via inheritance and the redistributive effects of various tax systems, including income, consumption, and proposed wealth taxes.

The model was further calibrated to the extreme initial conditions prevalent in South Africa, i.e., the top 1% holds 55% of wealth (Chatterjee et al., 2020, 2022), and reveals a stark policy paradox. A wealth tax is simultaneously a slow-acting tool for one goal and a fast-acting tool for another.

[The results below–and discussions thereof–are based on emergent results from the simulation models; please note that as we add further data and refine the models further, there might be minor changes to these estimates, but the overarching trends and narratives remain.]

Timeline 1: Targeting Slow-Moving Stock

The first emerging results confirm the central hypothesis: wealth distributions are extraordinarily sticky.

Even under a high wealth tax (3-7% annual rates on the top 1%), the simulation suggests that after 100 years, the top 1% wealth share would still be above 30-35%—a level higher than in most developed countries today.

Under a moderate wealth tax (1-3% annual rates), the top 1% share is estimated to decline by only a few percentage points after a full generation (25 years). After a century, it still remained exceptionally high, in the 40-45% range.

This quantifies the immense gravitational pull of accumulated capital. It demonstrates that if a wealth tax is framed only as a tool to rapidly "reduce the amount of wealth held by the elite," it is set up for political failure. It cannot deliver visible short-term changes in top wealth shares, risking disillusionment and making it vulnerable to the very political attacks seen in the UK.

Timeline 2: Achieving Fast-Flowing Revenue

In stark contrast to the slow-moving stock of wealth, the impact on the flow of public revenue is immediate and substantial.

From the very first year, the moderate tax (Scenario A) generated a stable and significant stream of annual revenue in the range of 1.5% to 2.0% of GDP for the synthetic population.

The high tax (Scenario B) generated even more, potentially 3.0% to 3.5% of GDP for the synthetic population annually.

This revenue stream remains predictable throughout the 100-year simulation. The policy could, therefore, be a resounding success from day one if the goal is to generate progressive revenue to fund public investment.

Concluding Remarks: A Pragmatic Pivot for Policy in a Contested Field

These simulation results indicate the need for a pragmatic pivot for the public and political debate on wealth taxation.

A wealth tax must be understood as having a dual objective:

A long-term, slow-acting stock objective: To gradually reduce the concentration of wealth and curb the self-perpetuating dynamics of capitalism.

A short-term, fast-acting flow objective: To generate significant, progressive, and stable public revenue.

Reframing the policy from a solely punitive measure to a pragmatic public finance tool is essential for political viability. It shifts the narrative from a zero-sum conflict over existing wealth to a positive-sum investment in shared prosperity. In the South African context, the R70 billion to R160 billion in annual revenue from a moderate tax could obviate the need for a regressive Value-Added Tax (VAT) hike—which disproportionately burdens the poor—and instead fund critical investments in education, healthcare, and infrastructure (Chothia et al., 2025).

This "dual objective" framework provides a crucial, evidence-based intervention in the live 2024 global policy debate. As the G20, led by Brazil, advocates for a tax on the stock of wealth, it faces technical criticism from bodies like the IMF. A March 2024 IMF note argued that taxing capital income (a flow) is "less distortive and more equitable" than taxing the wealth stock. Simultaneously, it faces political resistance at the national level, driven by narratives of "millionaire flight" (Hebous et al., 2024).

The emergent results from our ABM simulations present a potential bridge for such divides. They validate the IMF's concern that targeting the stock is a slow, multi-generational project (Timeline 1). However, they simultaneously validate the G20's proposal by demonstrating that a stock-based tax is the most immediate, stable, and powerful tool for generating a new progressive revenue flow (Timeline 2). This potentially pragmatic reframing—viewing the wealth tax as a public finance tool—provides the necessary foundation to advance a policy capable of funding shared prosperity while beginning the long, multi-generational journey of addressing the persistence of wealth.

References

Chatterjee, A., Czajka, L., & Gethin, A. 2022. Wealth Inequality in South Africa, 1993–2017. The World Bank Economic Review, 361, 19–36. https://doi.org/10.1093/wber/lhab012

Chatterjee, A., Czajka, L., Gethin, A., & UNU-WIDER. 2020. Estimating the distribution of household wealth in South Africa. WID.World Working Paper Series, 2020. https://doi.org/10.35188/UNU-WIDER/2020/802-3

Chothia, F., Rukanga, B., & Fihlani. 2025, April 24. South Africa reverses VAT increase that threatened ANC-DA coalition. BBC World. https://www.bbc.com/news/articles/cdrg2rve3vvo

Cohen, P. 2025, October 31. Are Wealth Taxes the Best Way to Tax the Ultra Rich? The New York Times. https://www.nytimes.com/2025/10/31/business/economy/wealth-tax-france.html

DIRCO. 2025, August 28. President Cyril Ramaphosa launches historic G20 experts taskforce led by Joseph Stiglitz to combat extreme wealth inequality—DIRCO. https://dirco.gov.za/president-cyril-ramaphosa-launches-historic-g20-experts-taskforce-led-by-joseph-stiglitz-to-combat-extreme-wealth-inequality/

Hebous, S., Klemm, A., Michielse, G., & Osorio-Buitron, C. 2024. How to Tax Wealth. International Monetary Fund. https://doi.org/10.5089/9798400266881.061

House of Commons. 2025, October 14. Treasury Committee, Oral Evidence: Budget 2025, HC1349. Parliament of the United Kingdom. https://committees.parliament.uk/oralevidence/16489/pdf/

Institute for Fiscal Studies. 2025, October 30. How to fix wealth taxes. Institute for Fiscal Studies. https://ifs.org.uk/articles/how-fix-wealth-taxes

Lustig, N. 2020. The “Missing Rich” in Household Surveys: Causes and Correction Approaches. SocArXiv. https://doi.org/10.31235/osf.io/j23pn

Partington, R. 2024, February 29. ‘A historic step’: G20 discusses plans for global minimum tax on billionaires. The Guardian. https://www.theguardian.com/news/2024/feb/29/taxation-worlds-billionaires-super-rich-g20-brazil

Piketty, T. 2014. Capital in the Twenty-First Century A. Goldhammer, Trans. Harvard University Press.

Saez, E. 2017. Income and Wealth Inequality: Evidence and Policy Implications. Contemporary Economic Policy, 351, 7–25. https://doi.org/10.1111/coep.12210

Stiglitz, J. E. 2011. Rethinking development economics. World Bank Research Observer, 262, 230–236. https://doi.org/10.1093/wbro/lkr011

Stiglitz, J. E. 2012. The Price of Inequality. WW Norton and Company.

Stiglitz, J. E., Abdenur, A., Byanyima, W., Ghosh, J., Valodia, I., & Zembe-Mkabile, W. 2025a. Report of the G20 Extraordinary Committee of Independent Experts on Global Inequality. G20.

Stiglitz, J. E., Abdenur, A., Byanyima, W., Ghosh, J., Valodia, I., & Zembe-Mkabile, W. 2025b. Technical Note: G20 Extraordinary Committee of Independent Experts on Global Inequality. G20.

Stiglitz, J. E., Abernathy, N., Hersh, A., Holmberg, S., & Konczal, M. 2015. Rewriting the Rules of the American Economy: An Agenda for Growth and Shared Prosperity. Roosevelt Institute.

Tax Justice Network, Partiotic Millionaires UK, & Tax Justice UK. 2025. The millionaire exodus myth: A critical reconsideration of the Henley & Partners Private Wealth Migration report. Tax Justice Network. https://taxjustice.net/wp-content/uploads/2025/06/The-millionaire-exodus-myth-A-critical-reconsideration-of-the-Henley-Partners-Private-Wealth-Migration-report-June-2025.pdf

Walt, V. 2025, September 15. The Wealth Tax Plans That Are Roiling New York and Paris. The New York Times. https://www.nytimes.com/2025/09/15/business/dealbook/wealth-tax-new-york-mamdani.html

WID.world. 2025, November 4. Statement from the World Inequality Lab on the G20 Extraordinary Committee of Independent Experts’ Report on Global Inequality. WID - World Inequality Database. https://wid.world/news-article/statement-on-global-inequality-stiglitz-report/

World Inequality Database. n.d. [Data set]. WID.World

Zucman, G. 2019. Global Wealth Inequality. Annual Review of Economics, 11, 109–138. https://doi.org/doi.org/10.1146/annurev-economics080218-025852

Zucman, G. 2024, May 3. It’s Time to Tax the Billionaires. The New York Times. https://www.nytimes.com/interactive/2024/05/03/opinion/global-billionaires-tax.html

Politicians and Wealth Reproduction

An international and interdisciplinary research project about politicians, policies and the reproduction of wealth